Is profitability in ride sharing and food delivery even possible?

Is profitability in ride sharing and food delivery even possible?

Innovation, profitability, and hope

Innovation and the sharing economy

Uber was once valued as much as $120 billion - the largest success story of the new wave of Silicon Valley startups. The company revolutionized the transportation industry using the dual marketplace model, which integrated “suppliers” and “consumers”. Uber was only liable for the tech in the middle.

Airbnb, which also did the same thing for the hotel industry, integrated homeowners and travellers on their tech marketplace. Airbnb and Uber are credited for popularizing the sharing economy: a peer-to-peer based economic model of sharing access to goods and services facilitated by a community-based online platform.

Uber has also had a big part in popularising the grow-and-burn-investor-money-till-you-take-over-the-world startup archetype. The company has never been profitable in its history:1

Doordash and other food delivery startups also see the same trend as Uber:

Tech startups not being profitable for years isn’t exactly something out of the ordinary. The idea is to grow (using incentives, improved user experience, data, etc.) to an incredible scale and operate almost monopolistically. For a tech company, costs shouldn’t increase at the same rate as revenue. It should theoretically cost as much to provide the tech based service to 10x the current user base. It should, at the least, not require 10x the cost.

Profitability and unit economics

The one assumption that needs to hold for ride sharing and food delivery companies to profit as they scale is positive unit economics - the profit they really make per ride/delivery. No matter the scale that these companies operate in, they will never be profitable if they’re not making a surplus per ride/delivery.

Accounting magic tricks: Adjusted EBITDA

On our path to unit economics, we can first take a look at silicon valley’s favorite magical figure - Adjusted EBITDA.

The idea for adjusted EBITDA is noble; we start off with EBITDA which is net income (earnings) with interest, taxes, depreciation, and amortization added back. This is a non-GAAP measure (it’s not generally accepted in accounting) but a lot of companies do report on it. We can see how reporting on EBITDA can be a problem - a good EBITDA can easily turn into net loss as these line items can be very large. This is true for tech companies as well since hardware depreciation can be a huge expense.

It gets shadier when we start adding more costs to make the EBITDA figure even more positive. Adjusted EBITDA adds in many more costs, one of which is stock based compensation. Stock based compensation is sometimes the main method of compensation for silicon valley execs.

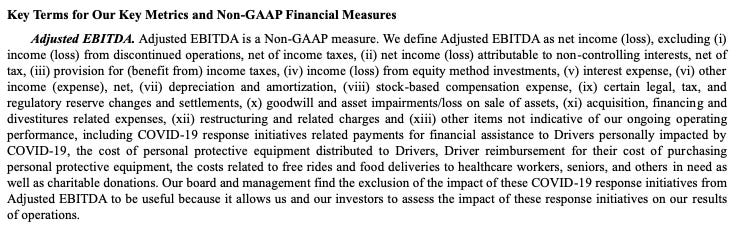

Uber defines Adjusted EBITDA as the following:

Critics of EBITDA and other non-GAAP accounting metrics have long argued that we can make any business look good when we start stripping out costs, especially when there’s no standardization. Just look at Uber’s definition above. Berkshire Hathaway’s Charlie Munger referred to Adjusted EBITDA as “bulls--t earnings” as a jab to silicon valley startups.

Let’s take Yelp. The review site reported net income of $17.2 million which is an EBITDA of $30.5 million. Add to that another $30.5 million in stock-based compensation, the primary way that CEO Jeremy Stoppelman gets paid, and Yelp ended up with adjusted EBITDA of $61 million. (CNBC)

Below is the part of Uber’s 2022 Annual Report where they offer the reconciliation of the non-GAAP Adjusted EBITDA to the GAAP measure of net loss. For Uber, their second largest contributor (we’ll get to the largest contributor a bit later) to Adjusted EBITDA was a stock based compensation of $1.8 Billion in 2022 (highlighted in yellow below). This won’t go away as Uber scales unless they stop offering employee stock ownership.

Another alarming figure is the $7 billion other expense figure above which comes as a result of the unrealized losses on debt and equity securities; Uber explains that this line item is due to the loss on their autonomous vehicle investments in Aurora and other unrealized losses on Grab, Didi, Zomato, etc. This (quite large) value has to be added back to net loss to get a positive Adjusted EBITDA value. We can still appreciate that this $7 billion figure is unrealized losses and isn’t as bad as the stock based compensation fiasco above.

But we can be optimistic. The idea for Adjusted EBITDA is to show a magical world where depreciation, amortization, unrealized gains on investments, and stock based compensation doesn’t exist. It’s what the business should be contributing to (at the same level) as it scales; all those other figures (depreciation, stock based compensation, etc.) shouldn’t scale at the same level, at least theoretically.

Adjusted EBITDA is also sometimes reported as a percentage of gross bookings2 by Uber (Adjusted EBITDA margin as a percentage of gross bookings was 2.4% in Q1 2023 for Uber). This ratio is also valuable to track as it’s supposed to represent efficiency; a high positive value would mean a large proportion of the money that users pay will actually generate “profits” for the company as it scales.

More shenanigans: contribution margins

Another non-GAAP measure that food delivery companies like Doordash like to use is contribution margin. Contribution margin is based on contribution profit - the money Doordash is left with when we take out all the direct expenses (all the variable costs). We can think of it as more aggressive Adjusted EBITDA.

We divide contribution profit by revenue to get contribution margin. Doordash’s exact definition is given below:

Essentially, we have to take out 2 quite large figures for Doordash (3 if we count depreciation and amortization) - research and development (R&D), and general and administrative (highlighted in yellow below). Nullifying these figures make contribution profit positive for Doordash for 2020-23.

This all leads to Doordash’s positive contribution margins of around 20% (see chart below).

Doordash is a tech platform and over $500 million in tech investment (R&D) in Q1 2023 has allowed them to generate a contribution profit of around the same amount. It’s very likely they’ll need to increase spending on R&D to remain competitive and allow them to increase take rates (more on this later). R&D will not go away; even in the most optimistic scenario of constant R&D costs, pure scale will not allow Doordash to overcome a potential $2 billion in R&D costs.

Take rates

Uber defines take rate as: revenue as a percent of gross bookings. It’s how much money Uber pockets from the money that users pay. This number, for users, is the marketplace tax. And it can be quite high as the report below shows:

What this means is that for any $100 trip in Q1 2023, users would need to price Uber’s value addition as $28.9 (both riders and drivers). This has caused a lot of controversy with Uber and more lawsuits to boot.

It’ll be interesting to see how the marketplace reacts to a larger take rate if Uber needs to go in that direction. Although, Uber did mention that long term take rate targets were lower at 25% on rides and 15% on deliveries in their 2022 investor day.

For Doordash, take rate is defined as revenue as % of gross order value (similar to gross bookings). This hovered at around 11% for the last few years (see chart below).

Unit economics

In order for Uber and similar services to actually become profitable, they’d need to tweak some (if not all) of those figures I mentioned above:

They’d need to scale and increase gross bookings/GMV/GOV3 - these companies need to scale and most of the adjustments needed to become profitable relies on being almost monopolistic e.g. increasing commissions and removing incentives. This would have to be backed up by any of the following points.

Revenues would need to increase - this would happen either by increasing prices, adding more fees or increasing the take rate (and taking a larger proportion of gross bookings/gmv/gov). This will largely depend on existing competition as users may stop using the app if the company charges them more. Suppliers/drivers may also opt out if they get charged a higher commission.

Adjusted EBITDA needs to increase as a % of revenue/gross bookings (or increase contribution margin)- the larger this figure this, the closer these companies get to becoming profitable. Note that, theoretically, as long as point 4 below holds, any positive adjusted EBITDA % of revenue/GB (or contribution margin) should result in net profits as the company scales (although a very low figure might require near impossible scale). The levers that can be pulled here are operational costs, R&D, marketing, etc.

Scale shouldn’t cause costs like stock based compensation to increase at the same rate.

Path to profitability levers

Hope and what the future holds

There is a path to profitability in these industries but it requires incumbents to take away the benefits they used to attract users; pricing and commission rates needs to increase and discounts need to be removed. There are still some (although not nearly as comparable) gains to be made in operational optimisation - reducing wastage, supply-demand prediction, better rider-user matching, routing algorithm optimisation, etc.

There is still a huge cost component that needs to be covered even with a positive contribution margin. Those costs e.g. stock based compensation, R&D, etc. need to be covered by the revenue the company is making. While scale alone can help the company to match these costs, the level of growth would be impossible for most of these companies to achieve. The better option might be a combination of growth and better unit economics.

Super app strategy

Uber is uniquely positioned compared to rivals such as Doordash in that they have multiple products. Uber has 3 main products - freight, mobility (rides) and delivery. These also have sub-verticals i.e. Uber for Business, grocery in Uber Eats, and last mile delivery via Uber Direct. Doordash and Delivery Hero also have some of these sub-verticals; they might offer last mile delivery or offer groceries but they do not offer completely different products.

The benefits in being leaders in each of these products is that Uber can create powerful integrations, cross promote products, and share user data between products. This leads to increased consumer lifetime spending, much lower acquisition costs (as Uber is just acquiring its user base from another vertical), operational efficiency via shared user data and a much better consumer experience. This is the super app strategy4 that Uber is banking on.

I think the benefits of a data moat5 are quite high for an industry with high competition and thin margins. I think this slide from Uber’s 2022 Investor Day really highlights the potential of the shared user data that Uber has:

Subscriptions and higher consumer spending

Another lever that these companies can use to drive higher consumer spending is subscriptions. DashPass, Uber One and Pandapro (for foodpanda, a Delivery Hero brand) all have the same proposition - recurring subscriptions for benefits such as free delivery.

Uber One takes this a step further by giving benefits in rides and delivery, which pushes cross product usage as well. If Uber could make every consumer order twice as much as they do now, scale would be much easier to achieve. Subscription models also allow companies like Uber to justify why they are charging higher prices for deliveries; Uber can push consumers to get the subscription to be charged lower delivery fees.

At the end of the day, this also needs to be priced such that Uber/Doordash/Delivery Hero make a profit per ride/delivery. Psychologically, it’s easier to drive up subscription costs versus increasing ride prices/delivery charges because it’s hard for consumers to break down the subscription costs per delivery/ride.

Advertising is another area that is being leveraged to create a new income stream. Adtech6 combined with the advertising spaces that Uber has (app screens, physical vehicles, couriers, etc.) can become a large part of Uber’s revenue.

The best part about this? There’s almost no direct costs for this so it’s just incremental profits.

Unique challenges in food delivery

Doordash unfortunately doesn’t have a rides section (or freight) to cross promote its products. This fact removes some levers they can pull to be profitable. Food delivery has a few unique problems that needs to be tackled before these companies can be profitable.

Scale hurts discoverability

The more restaurants and shops on a food delivery app, the harder it is for restaurants to stand out and make money. This problem can be monetized by food delivery apps using paid placements but this would hurt the restaurants who cannot keep paying to be promoted on the app; lower quality or smaller restaurants would be disincentivized to be on the platform.

Pricing power

Another issue is that, in contrast to ride sharing apps, food delivery apps cannot set food prices and can only take a chunk of it for themselves. This becomes a zero sum game for everyone - there is only a set amount of money that can be shared by the delivery app, the restaurant and the courier. This means that Doordash loses another lever to hit higher revenues.

Interestingly, restaurants do use this lever to keep up with Doordash’s high commission rates; increasing commissions can lead to markups on food delivery services where the restaurant charges more on the app vs their stores - something that can get quite ridiculous. This can impact orders negatively and may drive users to churn.

Value proposition

The value addition for ride sharing would be the digital marketplace that connects riders and drivers digitally - without it, alternatives aren’t as convenient. The value addition for food delivery would be a digital restaurant aggregator and delivery service - also extremely convenient. How much would an average consumer value these additions?

Imagine the scenario where a user discovers a restaurant on Doordash, looks up its menu, calls the restaurant’s own hotline, and asks them to deliver food to them. As long as the restaurant has their own delivery, the consumer saves money and Doordash gets absolutely nothing.

Most restaurants don’t have their own delivery (sometimes the restaurant’s own delivery is powered by a food delivery company) so Doordash might be safe from this for now. But we can see how a competitor service can knock Doordash off its perch by taking away the restaurant aggregator part of the value proposition.

From Uber’s take rates, we can see that the average consumer values the ride sharing proposition higher since Uber charges higher take rates on rides compared to delivery. This isn’t to say that ride sharing is invincible (it has its own quirks) but we can see the unique challenges that food delivery has. Ultimately, the value proposition is convenience and it’ll be interesting to see how much users are willing to pay for that in the future.

I personally think that some of these companies will be profitable - they’ll become a monopoly or an oligopoly in certain markets, charge higher commissions, remove incentives, charge higher prices and also scale. This will be driven by a lot of venture capital (VC) money.

Consumers will be annoyed at first. But for lack of choice and the benefit of convenience, they will still end up using these services. On the path to this future, a lot of these companies will lose money and the VCs will lose interest. Some of these companies will just fizzle out and their valuations will plummet. Others will be acquired by a larger company either overvalued or bought for scraps.

It’s unlikely that in such an industry everyone becomes a winner.

Unless we include the miracle profits in 2018 which happened due to sale of assets worth $3.2 billion. Without this, the company would have seen a net loss of $2.2 billion.

Gross Bookings is the total dollar value, including any applicable taxes, tolls, and fees, of: Mobility rides; Delivery orders (without discounts, tips and refunds); Driver and Merchant earnings; Driver incentives and Freight Revenue. Taken from Uber’s Q1 23 Earnings Press Release.

Gross Order Value (as used by Doordash) or Gross Merchandise Value (as used by Delivery Hero) means how much the consumer paid and is similar to Gross Bookings.

Super apps are mobile applications that combine several services. They keep the user within a single ecosystem of the services of a particular company. Most often these are mobile banking, lifestyle, delivery of goods, taxi ordering, and personal services. A popular example is WeChat in China.

Competitive advantage that a company gains by having exclusive access to unique and valuable data.

Advertising technology, also known as adtech, is an overarching term that describes the tools and software advertisers use to reach audiences, and deliver and measure digital advertising campaigns.